Progressive income tax: Money grab disguised as tax reform

By Lawrence McQuillan

The problem

In an interview with Huffington Post, Gov. Pat Quinn said that Illinois needs a progressive income tax.1 “That’s one of my goals before I stop breathing and I sure hope we can get that done in Illinois. Sooner rather than later,” he told the interviewer.

The same forces that helped Quinn land the governorship in 2010 and raise income taxes in 2011 are laying the groundwork for his progressive tax initiative. A progressive income tax (also called a graduated income tax) taxes individual income at ever-higher marginal tax rates as income rises.

State Sens. Michael Frerichs (D-Champaign), Kwame Raoul (D-Chicago) and Toi Hutchinson (D-Chicago Heights) have attended events in support of a progressive income tax. Also in favor of a progressive income tax are Senate President John Cullerton (D-Chicago) and Rep. Naomi Jakobsson (D-Urbana). Keith Kelleher, president of the Service Employees International Union (SEIU) Healthcare Illinois and Indiana, and Henry Bayer, executive director of the American Federation of State, County and Municipal Employees (AFSCME) Council 31, the largest union representing state government employees, also support a progressive tax.

Both the Illinois Education Association and the Illinois Federation of Teachers ask political candidates who take their 2012 candidate questionnaires if they would support a constitutional amendment on the ballot to implement a graduated income tax. And in January 2012, the liberal activist group Citizen Action/Illinois posted a job advertisement that read:

“Illinois’ major progressive forces, including its leading citizen activist groups, human services advocates and labor unions, are combining efforts to wage a multiyear battle for tax justice, culminating in a constitutional amendment referendum in 2014. We are seeking a . . . director of [a] statewide, three year legislative and referendum campaign to amend the Illinois Constitution and enact a graduated state income tax.”

This job position was filled in April 2012.

A union-funded group in Chicago, the Center for Tax and Budget Accountability (CTBA), has formalized a plan for a progressive income tax.

In February 2012, the CTBA released a report titled The Case for Creating a Graduated Income Tax in Illinois, which claims a “graduated income tax rate structure could reduce taxes for 94 percent of Illinois taxpayers and raise at least $2.4 billion more in revenue than the current five-percent flat tax.” But the truth is that a progressive income tax will mean higher taxes for middle-class Illinoisans and destroy needed jobs for the poor and working families.

Before Illinois’ flat income tax could be converted to a progressive tax, the Illinois Constitution would have to be amended. This is because its Revenue Article states: “A tax on or measured by income shall be at a non-graduated rate.” Currently, Illinois has a flat tax on personal income of 5 percent, which was increased by 67 percent in 2011 from the previous rate of 3 percent. Under current law, the increase will begin to sunset on Jan. 1, 2015 by falling to 3.75 percent, and then fall again to 3.25 percent on Jan. 1, 2025.

The CTBA and its allies are hoping to get approval for a progressive tax by three-fifths majorities in both chambers of the Illinois General Assembly – 36 senators and 71 representatives – to put the question to voters in a general election. Lawmakers would have to approve a progressive tax amendment by early May 2014 to be included on the November 2014 ballot. The earliest that a progressive tax could go into effect, therefore, would be 2015. But supporters are already laying the groundwork and beginning the campaign to get this measure on the ballot in 2014 and approved by either 60 percent of those voting on the question or a majority of those voting in the election.

The CTBA progressive tax plan circulating around the state would impose eight ever-higher marginal tax rates, topping off at 11 percent (see Table 1 below). This would tie Illinois with Hawaii for having the highest top income tax rate.

Supporters of the progressive tax are doing everything in their power to increase state spending now to justify no sunset of the 2011 tax hike and to be able to argue for even steeper progressivity in the future. These suggested marginal tax rates are only conversation starting points. In fact, the CTBA already favors state spending increases in excess of the $2.4 billion they hope to raise with the progressive income tax, meaning these marginal tax rates are only their starting points and will likely increase.

There are many myths underlying the CTBA scheme that will be exposed in this report, but a central myth is its claim that the plan would cut taxes for 94 percent of Illinois taxpayers. In reality, the CTBA scheme will increase taxes on 85 percent of filers because the plan assumes the 2011 income tax rate hike will not sunset as scheduled under current law. It is scheduled to fall to 3.75 percent in January 2015. But notice that the CTBA’s tax rates, which could not go into effect until 2015, use the current 5 percent rate, not the sunset 3.75 percent rate. CTBA’s tax rates also are higher than the rate in House Bill 175, a bill supported by 41 legislators in the 97th General Assembly that would repeal the 2011 tax hikes and return the personal income tax rate to the 2010 level of 3 percent.

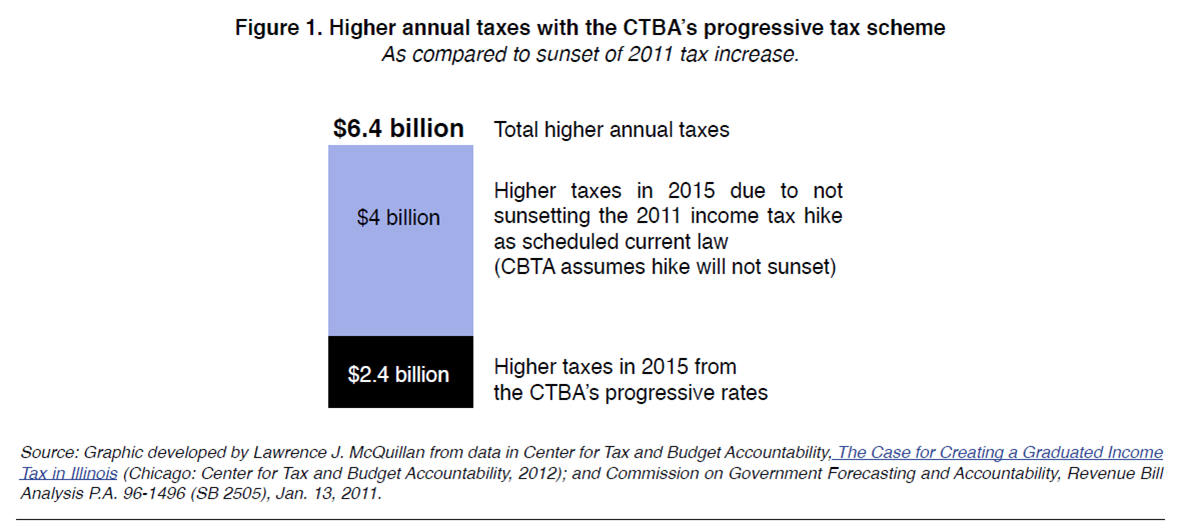

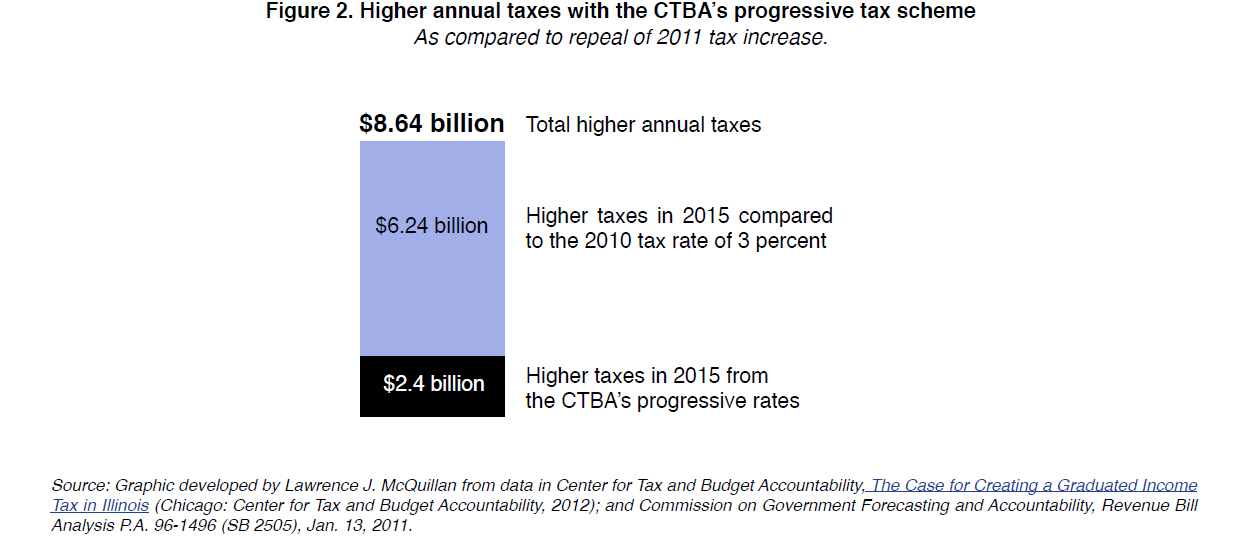

As a result of the 2011 temporary tax hikes being made permanent, the CTBA plan will actually raise taxes by $6.4 – 8.64 billion annually instead of the $2.4 billion they advertise (see Figure 1 and 2 below).

No state can tax itself to prosperity. A progressive income tax would be disastrous for the people of Illinois and the state’s economy because it would slow economic growth, kill jobs and make state budget deficits larger. It would be yet another anti-growth money grab to plague the state.

This report exposes the myths underlying the progressive tax and highlights its problems and pitfalls in three main sections:

(1) The national tax environment and competitiveness

- A progressive tax will send Illinois’ already high taxes even higher

- A progressive tax is being rejected by other states in favor of low, flat rates

(2) How the progressive tax hurts you

- A progressive tax will creep into the middle classes

- A progressive tax punishes success at ALL income levels

(3) How the progressive tax hurts the economy and state budgeting

- A progressive tax hurts job creation and economic growth

- A progressive tax is morally unfair, predatory and punitive

- A progressive tax is a recipe for budgeting disaster

Our solution

First, Illinois should discard any notion of enacting a progressive income tax of any kind. Instead, it should make its tax system more competitive by repealing the record 2011 income tax increase. On Jan. 1, 2011, the state’s individual income tax rate increased 67 percent to 5 ercent, from 3 percent. This tax hike, along with the corporate income tax increase also passed in 2011, should be repealed, returning nearly $7 billion annually to hard-working Illinoisans. The repeal should be done in conjunction with major spending reforms in public pensions, Medicaid and other spending programs as detailed in Budget Solutions 2013.37

Long term, the state should start a discussion about how best to abolish its personal income tax – joining nine states that do not tax personal income.

For most of this nation’s history, income taxes were unconstitutional. The 16th Amendment to the U.S. Constitution, ratified in 1913, gave the U.S. Congress the right to levy an income tax. The first Illinois income tax was signed into law by Republican Gov. Richard Ogilvie in 1969. Before then most state funding came from a statewide property tax, abolished in 1932, and a subsequent sales tax.

Abolishing the income tax doesn’t mean a lack of government revenue. Over the past decade, tax revenues in the nine states without an income tax have grown two times more than the nine states with the highest income tax rates (an average of 124 percent versus 62 percent).

Because productive economic activity is greater when there is no income tax, the tax base grows quicker to yield more tax revenue from the sales tax and property tax.

Why this works

Pro-growth policies best incentivize work, investment and upward mobility for all. Illinois should repeal the 2011 income tax hike and start a discussion on abolishing its personal income tax long term. These pro-growth steps would be good for family budgets, good for the state’s economy and good for the poor.

Good for families

Repealing the 2011 income tax hike would save the previously mentioned Illinois household with $50,000 of taxable income about $840 to $960 per year, the equivalent of a month or two of groceries.39 Repeal would also jump-start the economy, helping to lower the state’s unemployment rate.

Abolishing the state’s current 5 percent flat income tax completely would immediately save this Illinois household about $2,100 to $2,400 per year gross.40 People should be allowed to keep the fruits of their labor and invest in themselves or their businesses free from taxation. By not taxing labor income, Illinoisans would also bequeath a stronger economy to their children with more job opportunities.

Good for Illinois’ economy

States with low flat taxes or no income taxes have stronger economic growth and job creation and faster-growing populations. States with lower tax burdens, lower marginal tax rates, and less progressivity have more robust economies with strong incentives to live, work and start new businesses. Based on the results reported by Engen and Skinner discussed earlier, Illinois would boost its economic growth rate by between 0.2 and 0.3 percentage points if it scrapped its income tax entirely. This effect might seem small, but through compounding, it alone would cause living standards to double in 12 generations.

By not adopting a progressive income tax, Illinois can avoid further economic and budgeting disasters like those plaguing California, New York and New Jersey. Since 2000, the data shows that 1.2 million more people left California than moved there, the second biggest net loss after steeply progressive New York.41 Illinois should not copy Taxifornia’s uncompetitive, volatile tax system. Instead, Illinois should start a dialogue about abolishing its personal income tax.

Good for the poor

The progressive tax hike proposed by the CTBA would cut economic output in Illinois up to $26 billion and kill as many as 88,000 Illinois jobs, not create jobs from more government and consumer spending as the CTBA alleges.

This needless economic contraction would be devastating to the state’s poor, a group that has already suffered much during the Great Recession and would be first to lose their jobs from a progressive tax plan.

Instead of a progressive income tax, Illinois needs to lower its flat tax or eliminate the income tax. This will pave the way for more job creation and allow the poor to keep the fruits of their labor. A robust economy with rapid job creation is the best way to help the poor, who typically have fewer marketable job skills and thus tend to be laid off first during downturns.